Skip to content

Skip to content

A bounced check during check cashing happens when a bank or financial institution refuses to process the payment. This usually occurs because the account has insufficient funds, the account is closed, or the check details are incorrect. For customers, a bounced check can lead to fees, delays, and even legal consequences. For money services and financial providers, it triggers strict compliance duties, including reporting under BSA/AML rules. Understanding why checks bounce, what penalties follow, and how to prevent them helps customers avoid costly mistakes and ensures transactions remain safe, secure, and compliant.

Understanding Bounced Checks in Financial Services

A bounced check is more than just a payment mistake. It can trigger fees, compliance reporting, and even legal action.

What Is a Bounced Check?

A bounced check is a payment instrument returned unpaid by a financial institution. The funds are not released to the recipient.

Checks usually bounce for reasons such as:

- Insufficient funds in the issuer’s account.

- The account is being closed before deposit.

- Errors like mismatched amounts or incorrect dates.

- Expired checks not deposited within the valid timeframe.

Federal Rule: Under the Bank Secrecy Act, recordkeeping and identification are required for cash purchases of monetary instruments such as money orders and cashier’s checks when the total is between $3,000 and $10,000 in one business day. CTRs are required when cash transactions exceed $10,000 in one business day.

CTRs apply only to cash in or cash out transactions. A check deposit or check cashing by itself does not trigger a CTR unless it results in receiving or disbursing more than $10,000 in cash in the same business day.

Order Express Policy: As a safeguard, Order Express requires identification when customers cash checks of $3,000 or more. This is a company policy, not a federal requirement.

Why Do Bounced Checks Matter?

Bounced checks may look like small mistakes, but they have broader implications. A pattern of bounced checks can indicate fraud or financial distress. Money services are legally obligated to report suspicious transactions under the Anti-Money Laundering Act.

If structuring is suspected, providers must file Suspicious Activity Reports (SARs). Structuring means breaking large transactions into smaller ones to avoid ID verification or CTR reporting. For example, trying to cash multiple smaller checks to avoid detection is considered illegal.

Duties of the Check Issuer

The check issuer carries primary responsibility. Writing a bad check can lead to returned check fees, overdraft charges, and legal consequences. Knowingly writing bad checks may result in criminal penalties. The exact consequences vary depending on state law.

Check writers must also understand that providers monitor and report irregularities. Attempting to bypass reporting requirements exposes issuers to regulatory action. Providers must also ensure transactions are not linked to individuals or entities on the OFAC sanctions list.

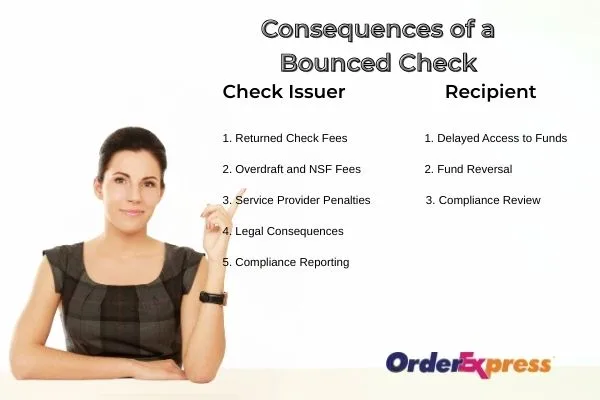

Consequences of a Bounced Check

The effects of a bounced check extend to both the issuer and the recipient. Providers also face obligations under Bank Secrecy Act and AML compliance.

Consequences for the Check Issuer

- Returned Check Fees

Banks may charge between $10 and $36 for each returned check. These fees add up quickly. - Overdraft and NSF Fees

If the account lacks funds, additional penalties like overdraft or NSF fees apply. Some banks waive them, but many still enforce them. - Service Provider Penalties

If a check was used for a bill payment, late fees may follow. Businesses may suspend service until payment clears. - Legal Consequences

Knowingly issuing a bad check can be treated as fraud. Repeat offenders may face fines or jail time. - Compliance Reporting

- Federal Rule: MSBs must file Suspicious Activity Reports (SARs) for covered activities such as money transfers, selling or redeeming money orders, or currency exchange when suspicious transactions involve $2,000 or more.

- Order Express Policy: For check cashing, SAR filing is voluntary under federal rules. Order Express may still file SARs voluntarily when suspicious or fraudulent check cashing activity is detected.

Consequences for the Recipient

- Delayed Access to Funds

Funds cannot be used until a replacement payment is issued. This delay can disrupt financial obligations. - Fund Reversal

If funds were released before the check cleared, the institution can reverse the transaction. Customers must repay any withdrawn funds. - Compliance Review

Recipients who repeatedly cash bad checks may be reviewed for suspicious activity. Providers must evaluate risk carefully to protect the financial system and meet consumer protection standards.

Compliance Obligations for Providers

Financial service providers follow strict reporting rules:

- Federal Rule: A CTR must be filed for cash transactions above $10,000 in a single business day. CTRs apply only to cash , not checks unless the transaction results in cash in or cash out over $10,000.

- Federal Rule: SARs are mandatory for certain MSB activities such as money transmission, selling or redeeming money orders, or currency exchange when suspicious transactions involve $2,000 or more.

- Order Express Policy: For check cashing, SAR filing is voluntary under federal rules. Order Express may still submit voluntary SARs when unusual or fraudulent check cashing activity is detected.

Structuring attempts must be reported and rejected immediately. These requirements protect the financial system and reduce opportunities for fraud. They also ensure customers are protected under the law and align with remittance transfer regulations.

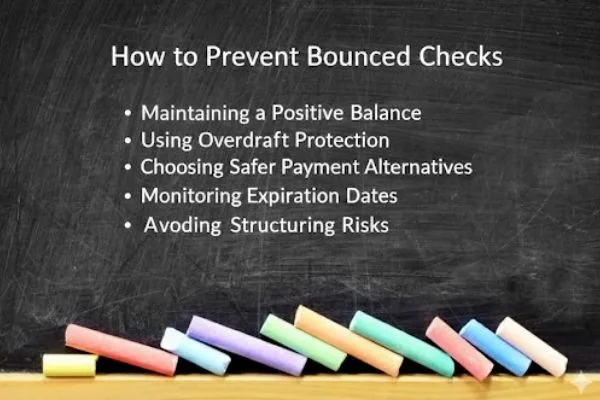

How to Prevent Bounced Checks

Preventing bounced checks benefits everyone. Customers save money, and providers reduce compliance risks.

Maintaining a Positive Balance

Always keep more funds in your account than you expect to use. A buffer of several hundred dollars helps prevent overdrafts.

Set up mobile alerts for low balances. Regular monitoring makes it easier to avoid bounced checks. Customers can also improve financial awareness by reviewing consumer banking guides.

Using Overdraft Protection

Many banks offer overdraft protection. Linked savings accounts or credit cards automatically cover shortfalls. While small fees apply, this option is safer than bouncing checks.

Choosing Safer Payment Alternatives

Some payment methods reduce the risks associated with checks:

- Certified checks guarantee the funds are available.

- Cashier’s checks provide bank-backed security.

- Money orders are prepaid and cannot bounce.

- Wire transfers and electronic payments clear almost instantly.

- Debit and credit cards provide reliable and secure payment options.

Order Express offers other financial services that can provide safer transaction options. Customers should also ensure they bring acceptable identification when cashing larger checks.

Monitoring Expiration Dates

Checks can expire if not deposited in time. Always cash or deposit checks promptly. Stale-dated checks are often rejected.

Avoiding Structuring Risks

Never split a large transaction into smaller ones to avoid reporting. This is structuring, and it is illegal.

Providers are required to file SARs if structuring is suspected. Customers should understand that compliance rules protect them, not hinder them. For instance, cross-border payments rely on strong KYC checks to ensure regulatory compliance.

Extra Guidance for Customers

Practical advice empowers customers and strengthens trust in money services.

Communicating with Check Issuers

Contact the check writer quickly if a payment bounces. Many cases are caused by oversight, not fraud. Prompt action can resolve the issue.

Documenting Transactions

Always keep transaction records, receipts, and copies of checks. Good documentation is essential for dispute resolution and compliance. For check cashing over $3,000, identification and transaction documentation are mandatory.

Understanding Reporting Rules

- Federal Rule: Identification and recordkeeping requirements apply to cash purchases of monetary instruments (such as money orders and cashier’s checks) between $3,000 and $10,000 in one business day. CTRs must be filed for cash transactions over $10,000 in one business day. A check deposit or check cashing does not by itself trigger a CTR unless it involves more than $10,000 in cash.

- Order Express Policy: For check cashing, Order Express requires identification for transactions of $3,000 or more. This threshold is a company policy, not a federal requirement. Customers should view these requirements as safeguards that protect the financial system and honest users.

Protecting Against Fraud

Fraudulent checks are common in online sales and among unfamiliar parties. Verify the source before accepting a check. Providers complete training to detect suspicious activity. Customers should also remain alert to avoid losses by reviewing fraud prevention resources.

Working with Trusted Providers

Always use licensed financial institutions or registered money services. These providers follow compliance laws and protect customer transactions. Unregulated services increase risks of fraud, loss, and non-compliance. Customers seeking support should contact Order Express for secure financial solutions.

Take control of your financial security. Avoid bounced checks, stay compliant, and use reliable services. Choose Order Express for trusted check cashing, money transfers, and secure solutions.

Conclusion

Bounced checks create significant challenges. They cause fees, delays, legal risks, and compliance obligations. For issuers, they can mean penalties and possible legal charges. For recipients, they cause lost time and reversed payments.

Check cashing providers add another layer by following strict compliance requirements. CTRs, SARs, and anti-structuring measures ensure the system stays safe.

Customers can protect themselves by maintaining account balances, using safer alternatives, and understanding compliance rules. By working with trusted financial institutions, they avoid risk and ensure safe transactions.

Reliable check cashing services do more than provide convenience. They protect customers and ensure compliance, offering a safer financial experience for everyone.

Disclaimer: This article is for general educational purposes only and does not provide legal or financial advice. Customers should contact their financial institution or compliance department for specific guidance on check cashing, reporting requirements such as CTR and SAR filings, and any state-level penalties that may apply.

Frequently Asked Question

Q1: What does it mean if a check bounces during check cashing?

A bounced check means the bank refused payment. Reasons include insufficient funds, closed accounts, errors, or expired checks.

Q2: What happens to the person who writes a bounced check?

The issuer may face:

- Returned check fees

- Overdraft or NSF charges

- Late payment penalties

- Impose legal consequences if authorities suspect fraud.

Q3: What happens to the recipient of a bounced check?

Recipients may experience:

- Delayed access to funds

- Reverse funds for early money release.

- Possible compliance reviews

Q4: How can I prevent a bounced check?

- Keep a positive account balance

- Use overdraft protection

- Deposit checks promptly

- Choose safer payment alternatives like cashier’s checks or money orders

Q5: Are there legal risks if a check bounces?

Yes. Authorities may treat knowingly issuing bad checks as fraud. Financial providers may also file Suspicious Activity Reports (SARs) when they suspect fraud or structuring.