Skip to content

Skip to content

A money order usually stays valid for six to twelve months, depending on the issuer’s policy. Some issuers may honor them longer but can deduct fees if left uncashed. Understanding these timelines is essential for anyone using financial services, such as check cashing, money transfers, or currency exchange. As a prepaid, guaranteed payment instrument, a money order provides a secure and accessible option within financial services, especially for customers without bank accounts who need to pay bills, send funds, or make reliable payments.

Understanding expiration rules, refund processes, and compliance requirements ensures customers avoid wasted money and protect transactions. Always confirm the issuer’s policy, keep receipts safe, and track your money order to stay in control.

Understanding Money Orders And Expiration Rules

Money orders continue to stand out as one of the most reliable prepaid payment tools available. They give customers peace of mind by guaranteeing funds, unlike personal checks that can bounce. This makes them an appealing option for individuals handling essential expenses such as rent, bills, and personal transactions. By securing the payment upfront, issuers ensure that recipients receive the promised amount without delays or surprises.

For many consumers, especially those without access to traditional banking, money orders are more than a convenience. They serve as a vital link in financial services, working alongside check cashing, currency exchange, and money transfer solutions. Customers rely on them for flexibility, security, and accessibility. Understanding how money orders function and when they expire helps customers make smarter decisions and safeguard their financial transactions.

What Is a Money Order and How It Works

A money order is a trusted form of payment that people use when they want security and assurance. It is purchased in advance, and the value is guaranteed, which means the recipient can deposit or cash it without worrying about insufficient funds. This makes a money order especially helpful when making important payments where reliability matters.

Many people choose a money order for everyday needs such as paying rent, settling bills, or sending money safely to another person. It provides more protection than carrying cash and avoids the uncertainty that can come with personal checks. By using a money order, you can complete transactions confidently and keep your payments secure.

Adding The Recipient’s Name On A Money Order

When completing a money order, always write the recipient’s name clearly in the space provided. This ensures the money order reaches the right person or business and prevents delays or rejections. Treat this step with care, because an incorrect name can cause issues when the money order is cashed or deposited. By filling in the recipient’s name accurately, you secure a smooth and reliable payment process.

Understanding The Entity Providing The Funds In A Money Order

The entity providing the funds is the person or group who pays for the money order upfront. This step guarantees that the money order is fully backed before it is issued, giving the recipient confidence that the funds are secure. By knowing who supplies the payment, customers can better understand how money orders work and why they remain a trusted way to send money safely.

Money Order Amount Explained

Every money order must show the exact amount to be sent, which makes it a secure and reliable payment option. By filling in the amount clearly, both the sender and the recipient know the funds are guaranteed. This helps prevent confusion, protects against errors, and ensures the money order can be cashed or deposited without delays. Understanding the role of the amount is an important step when using a money order for safe financial transactions.

Tracking A Money Order With Its Serial Number

Every money order includes a unique serial number that serves as both a tracking tool and a security feature. This number allows customers to confirm whether the payment has been cashed or remains pending. By keeping the serial number safe, you gain peace of mind and maintain control over your transaction. It ensures the recipient can confidently deposit or cash the money order, knowing the funds are already guaranteed.

Types Of Money Order Customers Should Understand

Money orders are a trusted payment method, but not all are the same. Different issuers provide unique advantages, and choosing the right option can help customers avoid delays or complications. Knowing the types of money order available gives you the confidence to pick the best fit for your payment needs.

Here are the most common types of money order you may encounter:

- Postal money orders are often used for domestic and international payments.

- Financial institution money orders come from banks or credit unions and are widely accepted.

- Retail or money service business money orders offer quick access for customers who may not have bank accounts.

Each type of money order serves a specific purpose, and understanding their differences helps you act with certainty. Postal money orders are ideal for sending funds securely across distances. Bank-issued options may provide more trust and recognition with businesses. Retail and service-based money orders give added convenience when traditional banking is not available. By comparing your options, you can make smarter decisions, protect your money, and ensure your payment reaches the recipient without issues.

Why Money Orders Matter In Financial Services

Money orders give customers a secure way to make payments without needing a bank account. They are a trusted option for people who want to send funds safely, cover bills, or handle personal payments. Because they are prepaid, money orders help individuals stay in control and avoid financial setbacks.

In financial services, money orders work alongside check cashing, money transfers, and currency exchange to create more flexible options for customers. This variety allows people to choose the service that best fits their needs. For those who want security and reliability, money orders remain a dependable solution that makes managing everyday transactions easier.

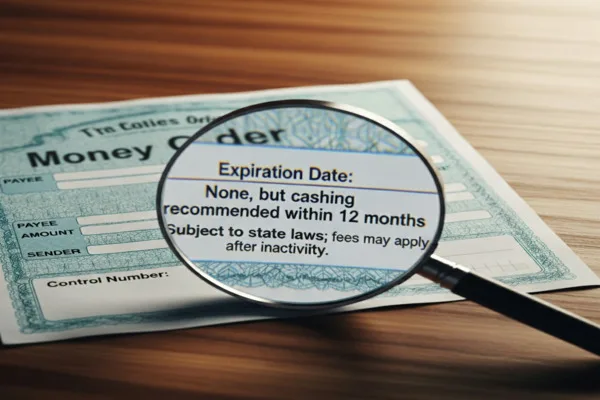

General Expiration Policies For Money Orders

Money orders are not valid forever, and most come with specific expiration periods. While many remain valid for six months to one year, the actual timeline depends on the issuer. Customers should always confirm the exact expiration date at the time of purchase to avoid delays or complications.

Keeping track of your money order is just as important as knowing its expiration. The serial number printed on each order allows customers to verify whether it has been cashed. Holding onto your receipt and monitoring the status ensures that you can act quickly if a refund or replacement becomes necessary. By staying proactive, you protect the value of your money order and avoid disruptions.

Sample Table: Money Order Validity and Fees

Since expiration timelines can vary depending on the issuer, it helps to have a quick overview of the most common practices. The table below compares typical validity periods, potential fees, and what you should expect from different issuers.

| Issuer Type | Typical Validity | Possible Fees if Left Uncashed | Key Notes |

| Postal Money Orders | 12 months (often longer) | Usually no expiration, but service charges may apply after 1 year | Popular for domestic and international payments |

| Bank or Credit Union Money Orders | 6-12 months | Dormancy or research fees may apply after expiration | Often widely accepted and trusted |

| Retail/Money Service Business (MSB) Money Orders | 6-12 months | Service fees deducted monthly after expiration window | Convenient for customers without bank accounts |

This comparison makes it clear that while most money orders stay valid for 6-12 months, fees and policies vary by issuer. The safest way to protect your funds is to cash or deposit your money order promptly and always confirm the terms at purchase.

How Issuers, Compliance, And Federal Rules Affect Validity

Money orders are subject to both federal compliance standards and issuer-specific policies, but these two areas serve very different purposes. Federal laws like the Bank Secrecy Act focus on identity verification, transaction reporting, and anti-money laundering controls. These measures apply to financial institutions and agents handling money orders, not to customers using them for everyday payments. They exist to safeguard the financial system and ensure transparency, especially for large or suspicious transactions.

Issuer policies, on the other hand, determine how long a money order remains valid and whether fees or refunds apply. These timelines are business decisions rather than legal mandates. Customers should understand that compliance rules govern reporting and monitoring, while expiration policies are set by the provider. Confusing the two can lead to costly mistakes, such as assuming a money order is valid indefinitely. Checking both federal obligations and issuer terms ensures smoother, safer transactions.

Federal Requirements And Reporting Rules

Federal law regulates how money services businesses handle money orders. Under the Bank Secrecy Act, transactions of $3,000 or more require identity verification. Transactions exceeding $10,000 in cash require filing a Currency Transaction Report. Suspicious activity requires a Suspicious Activity Report. These rules focus on anti-money laundering and terrorism financing prevention. They apply to issuers and agents, not consumers.

Order Express Compliance Program

Order Express follows all Bank Secrecy Act and USA Patriot Act rules. The company maintains training, monitoring, and reporting systems. Employees and agents must collect customer identification at certain thresholds. Compliance teams review suspicious patterns and submit reports when needed. These rules protect both customers and the company. Importantly, expiration timelines for money orders are not set by federal law or Order Express policy.

How Expiration Policies Differ From Compliance Rules

Expiration dates are commercial terms set by issuers. Federal rules govern reporting and identification but not expiration. Customers must distinguish between legal compliance and product rules. For example, identity verification applies to large purchases. Refunds or expiration depend on issuer terms. Mixing the two creates confusion. Always confirm issuer policies directly.

Practical Guidance For Customers Using Money Orders

Money orders continue to be a practical payment tool for customers who need a secure way to send funds. Whether you are paying rent, covering bills, or sending money to family, understanding how to manage money orders helps protect your money and ensures smooth transactions. Customers often rely on them when digital banking is not an option, which makes knowing the basics even more important.

From tracking an uncashed payment to requesting a refund for an expired order, customers have several options to safeguard their funds. Acting quickly, keeping receipts, and knowing alternatives such as digital transfers or check cashing services can make a big difference. With the right knowledge, handling money orders becomes simple, reliable, and stress free.

Important Compliance Reminder: For any money order purchase of $3,000 or more in 48 hours (or $1,000 in Arizona or Oklahoma), federal law requires customer identification. Customers must present valid government-issued ID (e.g., passport, U.S. driver’s license, consular ID) before completing the transaction. Always keep your receipt and serial number safe.

How To Track And Cash Money Orders

A money order always comes with a unique serial number that acts like a digital fingerprint. Customers can use this number to confirm if the money order has been cashed or is still pending. Tracking provides peace of mind and ensures that funds reach the right recipient. If the money order remains uncashed, the purchaser can usually request a replacement or ask for the money to be returned.

When it is time to cash a money order, customers have several safe options. It can be deposited at a financial institution, redeemed at a money service location, or handled at a retailer that processes payments. Some transactions are completed quickly, while others may require a short waiting period. Knowing how to track and cash a money order makes the entire process smooth and secure.

How Long Does A Money Order Take To Cash

The speed of cashing a money order depends on where it is presented and how it is verified. Many locations process them immediately, giving customers access to funds on the spot. However, some situations require more time, especially when the money order is deposited into an account rather than cashed directly.

Knowing how long a money order takes to clear helps people manage bills, rent, and personal expenses with confidence. If quick access to funds is needed, cashing in person is usually the best option. Depositing may take longer, but it provides extra convenience for account holders. Customers can reduce stress by keeping receipts, tracking the transaction, and asking about processing times before completing their payment. This knowledge turns money orders into an efficient tool rather than a source of uncertainty.

Instant Cashing For Money Orders

Many customers prefer instant cashing because it provides immediate access to funds from a money order. In most cases, financial institutions or service locations verify the details on the spot and release the money without delay. This quick process makes money orders a dependable choice for urgent payments or time-sensitive needs. Instant cashing also helps reduce the uncertainty that sometimes comes with other payment methods. By presenting a valid money order, customers can walk away with cash in hand on the same day. This convenience highlights why money orders remain a popular option for those seeking both security and speed in financial transactions.

Money Order Waiting Time

The waiting time for a money order depends on where you decide to cash or deposit it. Some places release funds immediately, while others need more time for verification. Knowing what to expect prevents delays in paying bills or completing important transactions. If a money order comes from a different provider, the waiting time is usually longer. In many cases, it can take one to three business days to clear. Planning ahead and keeping your receipt helps you track the process and avoid unnecessary stress while waiting for your money.

How To Cash A Money Order At Post Offices

Cashing a money order at a post office is often a straightforward process. Most transactions are completed quickly, giving customers easy access to their funds. Depending on how busy the location is, the process may be finished within the same business day. This makes post offices a convenient choice for those who prefer simple and reliable service. For customers who want fast access to money, post offices remain a trusted location to complete a transaction. The process requires presenting the money order and proper identification before the funds are released. By using a post office, customers can handle money orders with confidence, knowing their payments are processed securely and efficiently.

Refunds For Expired Or Lost Money Orders

When a money order expires, customers may still have options to recover their funds. Most issuers allow refunds if the original receipt and serial number are available. These details help confirm ownership and speed up the process. Acting quickly makes it easier to resolve the situation and ensures your money remains protected.

If a money order is lost or stolen, reporting it right away is essential. Prompt action reduces the risk of fraud and improves the chances of receiving a replacement. Always store your receipt in a safe place and track the money order when possible. Taking these steps gives customers peace of mind and confidence when using money orders for secure payments.

Fraud Prevention Tips from Order Express:

- Only purchase or send money orders to people or businesses you know.

- Never send money to someone you met online or to unknown callers.

- Safeguard your receipts and do not share your serial number.

- If you believe someone is trying to scam or defraud you, contact Order Express immediately at 1-888-666-1602.

Alternatives To Money Orders

When customers need to move money quickly, there are several alternatives to money orders that can help. Digital transfers and online wallets allow fast transactions and work well for those who already use bank accounts. These tools make it easy to send money almost instantly, offering convenience and accessibility.

However, money orders remain a dependable option for customers who prefer a paper-based payment or who do not use digital banking. They provide a secure way to cover rent, bills, and personal obligations. Choosing between money orders and other methods depends on individual needs, comfort level, and access to financial services.

Conclusion

Money orders remain a secure and dependable way to send funds, but their validity depends on the issuing provider. Most expire within six to twelve months, and refunds often require receipts and serial numbers. To protect your money, always confirm expiration timelines before purchase, keep records safe, and act quickly if issues arise. Federal compliance rules regulate reporting and identification, but they do not control expiration dates. Customers should separate compliance requirements from issuer terms to avoid confusion. If you need a flexible payment method, weigh money orders against digital transfers or other financial services. Take control today by reviewing your options, safeguarding your transactions, and visiting your financial services provider for expert guidance.

Disclaimer: This article is for general informational purposes only. Expiration dates, refunds, and processing times depend on the issuing provider. Federal rules govern compliance obligations but do not set expiration timelines. Customers should confirm terms directly with the money order issuer.

Order Express complies with all applicable Bank Secrecy Act (BSA), USA Patriot Act, and OFAC requirements but does not control issuer-specific validity policies.

If you suspect fraud or have a complaint, please contact Order Express Customer Service at 1-888-666-1602 or customer.service@orderexpress.com.

Call to action: Protect your money and stay informed. Visit your local financial services provider to confirm expiration policies and explore secure options for money orders, check cashing, and money transfers today.

FAQs

How long is a money order valid?

Most money orders stay valid for six to twelve months. Always check the issuer’s policy for exact expiration timelines.

What happens if a money order expires?

Expired money orders may be refundable. Keep your receipt and serial number. Contact the issuer for reissue or refund.

How can I track a money order?

Use the serial number. Check with the issuer’s website, call customer service, or visit the purchase location.

What do I need to cash a money order?

Present the money order and valid ID. Cash at a bank, credit union, retailer, or money services business.

What steps should I take if a money order is lost or stolen?

- Locate the receipt and serial number

- Contact the issuer immediately

- File a replacement or refund request

- Pay any processing fee