Skip to content

Skip to content

Cross-border payments come with significant fraud risks such as money laundering, social engineering, cybercrime, and transaction laundering but top financial service providers implement layered protection measures to keep them secure. These include strict Know Your Customer (KYC) and Know Your Business (KYB) checks, real-time transaction monitoring, enhanced identity verification, and compliance with Bank Secrecy Act (BSA) and Anti-Money Laundering (AML) regulations. Programs like Order Express’s BSA/AML Corporate Compliance Manual require ongoing staff training, risk-based reviews, and reporting of suspicious activity. Together, these tools help detect fraud early, protect customer data, and ensure compliance across international borders.

To stay ahead of evolving threats, providers must study current fraud trends and apply tested security measures. These include multi-layered security systems, continuous employee training, and alert-based monitoring of transactions. These practices align with key compliance sections in the Order Express program: Section 5 (General Compliance), Section 6 (KYC), and Section 11 (Suspicious Activity Reporting). Staying compliant with these guidelines helps protect both the provider and the customer from growing fraud risks in cross-border payments.

How Cross-Border Payments Fraud Happens

Understanding how fraud works is key to preventing it in cross-border payments. Criminals use a range of tactics to trick systems and people. One of the most common methods is social engineering.

Tactics Fraudsters Use in Cross-Border Payments

Fraud in cross-border payments often involves forged documents or deceptive transaction behavior. These methods are designed to bypass compliance checks and hide illegal activity.

- Social Engineering: Fraudsters use phishing, pretexting, and similar tactics to trick people into revealing sensitive information. These schemes target employees, agents, or customers, often by posing as trusted sources. Even with strong technology, human error can open the door to fraud.

- Order Express addresses these risks under Section 15.2 of its compliance manual. To reduce vulnerabilities, financial institutions must train staff and agents to recognize and resist manipulation. Regular awareness programs help employees identify scams before they cause harm. For guidance on consumer protection and fraud prevention, resources like the FTC Scam Alerts provide valuable tips.

- False Documentation: Fraudsters may use fake invoices, licenses, or contracts especially in countries with weak regulations, often backed by shell companies. To prevent this, institutions must enforce strict KYB checks. Sections 6 and 7 of the Order Express manual stress verifying business details, particularly for international clients.

- Transaction Laundering: Illicit funds may be funneled through legitimate accounts to make them appear clean. Fraudsters often disguise these activities under the cover of e-commerce or digital services. Monitoring for unusual transaction behavior is critical. Under the U.S. Bank Secrecy Act Travel Rule, we must collect, retain and transmit sender and recipient details on any cross-border transaction that totals more than USD 3,000 within a single business day.

- According to Sections 4.6 and 11 of the Order Express compliance manual, financial service providers should track sudden spikes in transaction volume or patterns that don’t match the customer’s typical activity. Detecting these red flags early can prevent further misuse of the payment system. For more on AML regulations, see the FinCEN website.

Other Common Cross-Border Payment Threats

Cross-border payment systems can also be used to fund illegal activities or steal sensitive information. Financial institutions must stay alert to these serious threats.

- Terrorist Financing: Funds are often moved through layers of fake transactions or nonprofit organizations acting as covers. These methods help hide the true source and purpose of the money. To detect such activity, providers must use OFAC screening and enhanced transaction monitoring. Section 27 of the Order Express manual outlines procedures for identifying, blocking, and reporting suspicious transfers tied to terrorism. The Consumer Financial Protection Bureau’s Remittance Transfer Rule resources offer further guidance on compliance requirements.

- Cybercrime: Cybercriminals target financial systems to gain unauthorized access or steal data. They may use phishing emails, ransomware, or advanced persistent threats. These attacks can lead to major breaches and loss of customer information. Sections 5.1 and 31 of the Order Express compliance manual stress the importance of using strong encryption, network security measures, and real-time system monitoring. Keeping digital systems secure is a core part of fraud prevention in cross-border payments. The TSA’s guidelines on travel security and identification also highlight best practices for identity verification.

Modern Fraud Risks in Cross-Border Payments

As financial technology evolves, fraud tactics also become more advanced. Virtual currencies and identity manipulation are two growing threats that demand extra attention.

- Virtual Currency Scams: Fraudsters often use crypto for Ponzi schemes, exit scams, and fake ICOs usually via unregulated platforms that are hard to trace. Providers must apply sanctions screening throughout and be cautious with non-cash instruments. Section 30 of the Order Express manual requires strict oversight when onboarding customers using virtual currencies, and any dealings with unregulated crypto exchanges must prompt an immediate risk review. For more on virtual currencies and IRS guidance, see the IRS Virtual Currencies page and Blockchain.com learning portal.

- Synthetic Identity Theft: In this scheme, criminals create fake identities by combining real and fake personal information. These identities are used to open accounts or secure unauthorized credit. To counter this, Section 7 of the Order Express compliance manual requires strong identity checks. Financial institutions must verify multiple data points and use advanced document validation tools. This multi-layered approach helps prevent fraud at the account opening stage and beyond.

- Protecting Against Malware Attacks in Cross-Border Payments: Malware such as spyware, ransomware, and keyloggers pose serious risks to cross-border payment systems. These attacks can steal sensitive data or allow unauthorized access to financial networks.

To protect against malware, institutions should use robust endpoint protection, conduct regular audits, and train staff to spot phishing. These practices align with Sections 5 and 23 of the Order Express manual on cybersecurity controls.

As threats evolve, ongoing system monitoring and employee training are essential. Suspicious Activity Reports (SARs) must be filed promptly, per Section 11. Currency Transaction Reports (CTRs) are required for cash transactions over $10,000, while SARs apply to any amount flagged as suspicious. For the latest on fraud trends, see Fintech Futures – PayTech.

Understanding the Risks of Cross-Border Payment Frauds

Cross-border payment fraud presents unique challenges that require specialized attention. Traditional compliance approaches may not fully address these risks in an international context.

One major issue is non-uniform regulations. Different countries have varying rules and enforcement levels. Some jurisdictions have weak anti-money laundering (AML) controls or data protection laws that make thorough Know Your Customer (KYC) checks difficult. Section 30 of the Order Express manual highlights the importance of strict onboarding and monitoring of foreign agents. It sets clear documentation standards and risk-based review procedures to help manage these regulatory differences effectively. Understanding these complexities is key to building a strong cross-border fraud prevention strategy.

Language and Cultural Differences

Communication barriers and cultural misunderstandings can make it harder to detect fraud in cross-border payments. These gaps may lead to errors or missed warning signs. To reduce this risk, institutions should provide localized training, employ bilingual support staff, and use standardized documentation. Section 5.3 of the Order Express manual outlines these best practices to ensure consistent and effective due diligence across regions.

Complexity of Cross-Border Transactions

Cross-border payments often involve many intermediaries, variable settlement times, and changing exchange rates. This complexity can hide money laundering techniques such as layering. Order Express tackles this challenge with detailed monitoring rules described in Section 4.6. The program also applies stricter scrutiny to nested or interconnected transaction relationships, helping identify suspicious activity more accurately.

Challenges from Incomplete Customer Information

Cross-border payments often face problems with missing or unverifiable customer data. This issue is especially common in countries without reliable public records. Sections 6 and 7 of the Order Express manual require collecting additional documents, such as proof of address and business registration. These documents must be obtained during onboarding and updated regularly to ensure accuracy.

Keeping Up with Technology Risks

Fraudsters take advantage of new payment platforms and decentralized finance (DeFi) tools before regulations catch up. To address this, Order Express continuously reviews emerging technologies. Section 31.2 covers updates to audit trails and risk detection models, ensuring the system adapts to new threats.

By understanding these risks, financial institutions can strengthen compliance efforts, flag high-risk transactions for closer review, and foster a strong culture of due diligence. This proactive approach helps protect cross-border payments from evolving fraud.

Common Challenges for Businesses and Financial Institutions

Even with clear compliance frameworks, putting them into practice can be difficult.

Limited Resources

Small businesses and independent agents often lack dedicated compliance teams or advanced fraud detection tools. To support these groups, Order Express provides centralized oversight. This includes regular audits and clear escalation procedures. These measures help ensure that even organizations with limited resources meet regulatory requirements and maintain strong fraud prevention. For related services, see Order Express Money Transfer and Check Cashing Services.

Expertise Shortfalls

Detecting advanced fraud requires skilled analysts and investigators. Order Express requires all staff to complete initial and ongoing AML training as detailed in Section 3.1. The program also offers additional support and remediation for agents who need improvement, outlined in Section 3.2. This ensures the team stays equipped to handle evolving threats.

Data and Analytics Challenges

Poor data quality or lack of integration between systems can weaken fraud detection efforts. Section 4.4 emphasizes maintaining thorough and accurate records. Sections 29.5 to 29.9 set standards for system integration and data hygiene. Following these guidelines helps create a reliable data environment that supports effective fraud prevention and compliance.

Balancing Security and Customer Experience

Strict security measures can sometimes create friction, leading to customer frustration. The Order Express program focuses on balancing strong fraud controls with smooth customer service. Automating compliance checks reduces the burden on users while maintaining protection. To enhance customer service, providers often integrate courier services and vehicle services for added convenience.

Navigating Regulatory Changes

AML regulations differ by country and often change faster than technology evolves. Order Express manages this challenge by regularly updating policies and aligning with FinCEN and OFAC guidelines. This approach ensures consistent compliance across all agents, no matter their location.

By combining technology, centralized oversight, and ongoing training, Order Express supports agents in overcoming operational hurdles while maintaining full regulatory compliance.

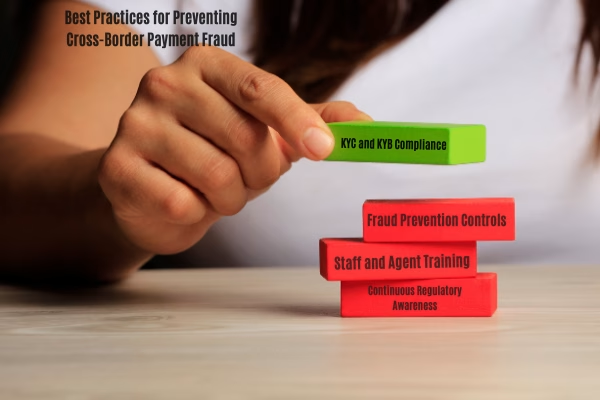

Best Practices for Preventing Cross-Border Payment Fraud

Order Express recommends several key AML best practices to help agents and employees prevent cross-border payment fraud effectively.

1. Multi-Layered Security Controls

Implement strong authentication methods such as biometrics and one-time passwords (OTP). Use endpoint protection, geolocation tracking, and fraud alert systems to detect unusual activity. Internal audits and incident response plans, detailed in Sections 15.1 and 29.3, ensure security measures stay effective and up to date.

2. Routine Risk Assessments

Regularly assess risks related to customer segments, agent activities, and transaction types. Section 31.6 requires scoring agents by risk level, with higher-risk groups subject to increased monitoring and controls. This helps focus resources where fraud risks are greatest.

3. KYC and KYB Compliance

Verify identities using government-issued IDs, beneficial ownership information, sanctions list screening, and document authentication tools. These steps, outlined in Sections 6 and 7, are vital to confirm the legitimacy of customers and businesses.

4. Real-Time Transaction Monitoring

Monitor transactions for suspicious patterns such as structuring, sudden spikes in activity, or transfers to high-risk countries. Section 4.6 includes automated alerts and behavioral models designed to identify anomalies quickly, enabling timely intervention.

5. Fraud Prevention Controls

Conduct regular inspections and quality assurance reviews of documentation submitted by agents. Proper recordkeeping and immediate reporting of any issues are required under Sections 29 and 30. These controls help maintain data integrity and regulatory compliance.

6. Continuous Regulatory Awareness

Keep training content updated with guidance from FinCEN, OFAC, and state regulators. Documentation of training programs, as required by Section 5.3, ensures staff remain informed on the latest compliance requirements.

7. Staff and Agent Training

Mandatory annual training prepares staff to recognize fraud typologies, red flags, and reporting responsibilities. Section 3.2 requires passing assessments to retain system access, ensuring ongoing competence.

By following these practices, institutions enhance compliance and build stronger defenses against fraud in cross-border payments.

Consequences of Cross-Border Payment Fraud

Undetected cross-border payment fraud can lead to significant and wide-ranging impacts on financial institutions and their customers. Understanding these consequences highlights why strong fraud prevention is essential.

- Financial Losses: Fraud results in direct monetary losses, including chargebacks, stolen funds, and costs related to account recovery. Additionally, institutions may face penalties for regulatory non-compliance, increasing financial strain.

- Reputational Damage: News of fraud incidents can severely damage an institution’s reputation. Loss of consumer and partner confidence makes it harder to attract and retain clients, affecting future business prospects.

- Legal Risks: Failing to meet filing requirements for Suspicious Activity Reports (SARs) and Currency Transaction Reports (CTRs), as detailed in Sections 10 and 11, exposes institutions to enforcement actions. Such non-compliance can lead to license suspension or revocation, limiting the ability to operate.

- Service Disruptions: Fraud detection may trigger frozen accounts, delayed transfers, and heightened scrutiny from regulators. These disruptions harm the customer experience and can interrupt normal business operations.

- Lost Partnerships: Institutions labeled as high-risk may lose strategic business partners. This loss restricts growth opportunities and limits access to key markets.

- Data Breaches: Ineffective protection of sensitive information can result in data breaches. These breaches lead to identity theft, additional fraud, and costly lawsuits, as covered under Section 23.

- Regulatory Sanctions: Financial penalties and public naming by regulatory bodies can damage an institution’s credibility and market position. Sanctions may also reduce operational capacity.

By following the BSA/AML compliance framework and applying risk-based controls, Order Express reduces both the likelihood and severity of these outcomes. This proactive approach strengthens institutional resilience and helps maintain secure, compliant cross-border payment services for all clients.

Conclusion

Cross-border payment fraud poses significant risks to both providers and customers. Staying protected requires robust fraud prevention measures and compliance with regulations. Financial institutions must implement multi-layered security, rigorous KYC/KYB processes, and real-time transaction monitoring. Regular staff training and continuous risk assessments help detect evolving threats early. Addressing challenges like complex regulations, language barriers, and technology risks is essential for effective fraud control. By following these best practices, providers can reduce financial losses, protect their reputation, and maintain customer trust. Consistent adherence to compliance frameworks, like those outlined by Order Express, ensures safer and more reliable cross-border payments. For any questions or support, providers and customers are encouraged to contact us. Taking proactive action today strengthens resilience and supports secure global financial transactions tomorrow.

Disclaimer: No security program can guarantee the complete elimination of fraud. The controls described here reduce – but do not eliminate – risk.

Frequently Asked Questions

What fraud protections should I expect from a cross-border payment provider?

Expect multi-layered security, strict KYC/KYB checks, and real-time monitoring. Providers should also train staff to spot fraud tactics and report suspicious activity promptly.

How do fraudsters exploit cross-border payment systems?

They use social engineering, false documents, transaction laundering, and cybercrime to bypass controls. Advanced scams involve virtual currencies and synthetic identities.

What role does staff training play in preventing fraud?

Training helps employees recognize phishing, social engineering, and suspicious transactions. Continuous education ensures up-to-date awareness of evolving fraud risks.

How do providers handle regulatory differences across countries?

They apply risk-based controls and strict onboarding protocols. Compliance frameworks are regularly updated to meet FinCEN, OFAC, and local regulations.

What are the consequences of undetected cross-border payment fraud?

Consequences include financial losses, legal penalties, reputational damage, service disruptions, lost partnerships, data breaches, and regulatory sanctions.

Federal law requires that customers for certain transactions be identified by name, address, government-issued identification and other relevant information.

You may be asked to provide this information to comply with the law.

© 2025 Order Express Inc. – Content approved by the Compliance Department on 7/28/2025.